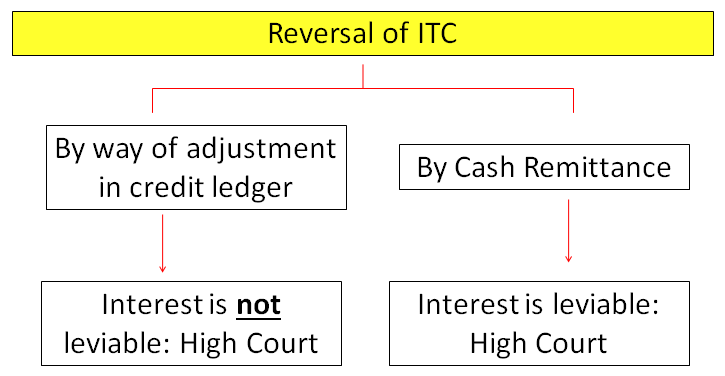

Reversal of ITC by petitioner through cash remittance is very well subjected to levy of interest: High Court

Reversal of ITC by petitioner through cash remittance is very well subjected to levy of interest: High Court

Though interest on reversal of ITC by way of adjustment in credit ledger is set aside by High Court.

Brief of Case

The challenge is to order dated 27.01.2021 levying interest under Section 50 of the CGST Act relating to both interest on cash remittances as well as remittances by way of adjustment of electronic credit register.

As far as the reversal by way of adjustment of credit ledger is concerned, it is covered by a decision in the case of Maansarovar Motors Private Limited V. The Assistant Commissioner. Both learned counsel concur on the position that in the light of the aforesaid decision, the levy to this extent is to be set aside and it is hence accordingly set aside.

As far as levy of interest on cash remittance is concerned, learned counsel for the petitioner only relies on the provisions of Section 42 of the Act which provides for a notice to be issued by the Assessing Authority in the case of mismatch of particulars at the end of the assessee, vis-a-vis, particulars/details furnished in the returns of the selling/purchasing dealer.

In this case, the provisions of Section 42 are not relevant, insofar as the impugned order itself records that the assessee has, on receipt of intimation of the wrongful claim of input tax credit (ITC), accepted the error in claim and has reversed ITC, both attributable to CGST and SGST through voluntary payment of tax in Form GST DRC-03.

The provisions of Section 42 can only be invoked in a situation where the mismatch is on account of the error in the database of the revenue or a mistake that has been occasioned at the end of the revenue. In a case where the claim of ITC by an assessee is erroneous, as in this case, then the question of Section 42 does not arise at all, since it is not the case of mismatch, one of wrongful claim of ITC.

As far as the levy of interest on belated cash remittance is concerned, it is compensatory and mandatory and the levy is upheld to this extent.

Comments

Post a Comment